There is a fundamental misalignment in the art world that is becoming more urgent as artistic subjectivity is increasingly commodified and democratized.

This is not simply a shift in market dynamics. It is a structural change in how culture is produced, circulated, and remembered.

Collectors often believe they are participating in a market, acquiring objects, expressing taste, and building private collections.

But that framing is incomplete.

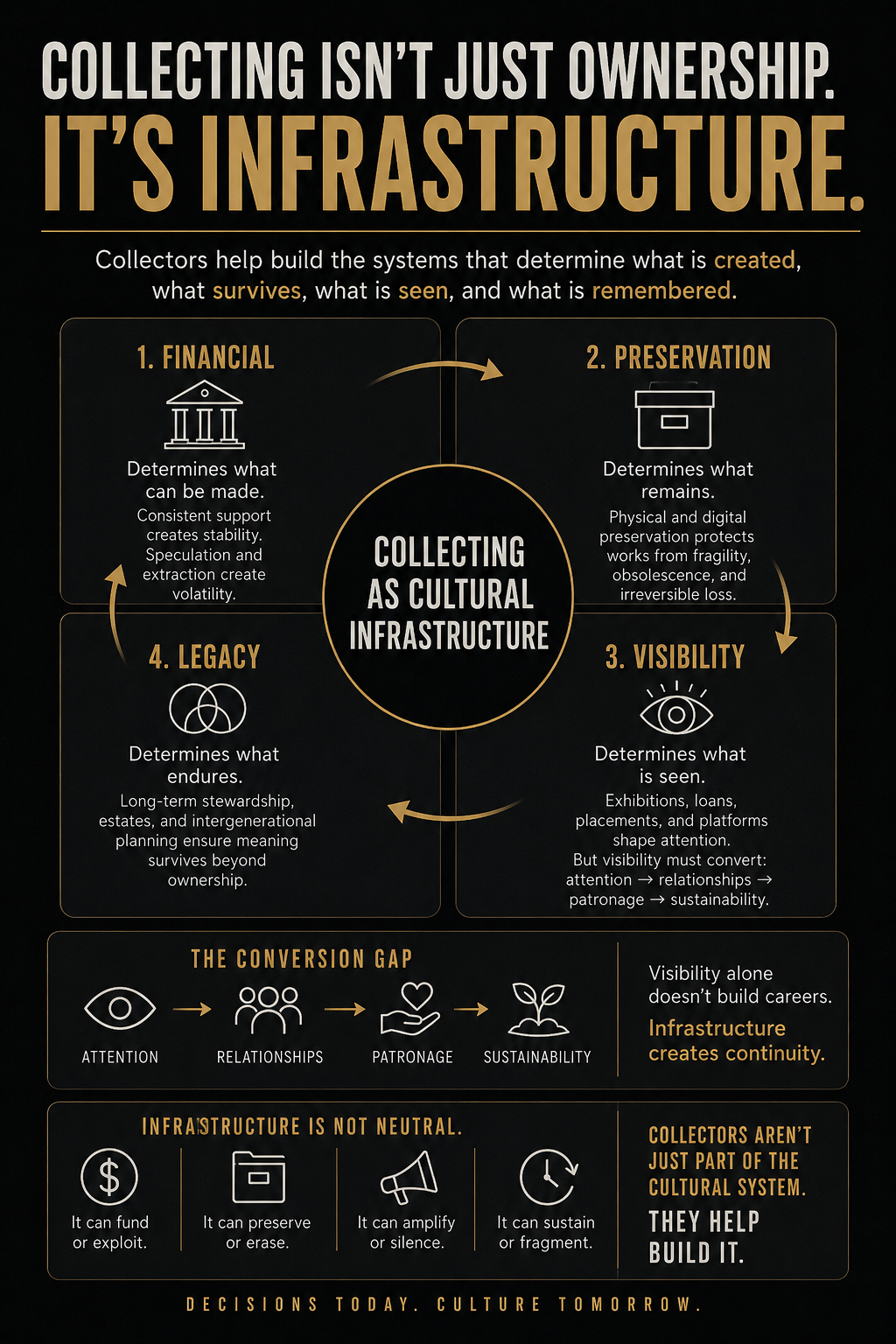

Collecting is not passive participation.

It is infrastructure.

Not physical infrastructure like roads or buildings, but cultural infrastructure: the systems that determine what is sustained, what is visible, what is preserved, and what is forgotten.

But infrastructure is not built through isolated actions.

It is built through repeated decisions over time that accumulate into structure.

And this infrastructure is not evenly distributed.

It is weighted.

Some actors disproportionately determine outcomes. One major collector placing a work in a museum can shape cultural visibility more than hundreds of private acquisitions combined.

Democratization expands participation, but it does not distribute influence equally.

Which means responsibility is not symbolic.

It is structural.

1. Financial Infrastructure

Financial infrastructure determines whether an artist’s practice can continue over time.

Artists do not work in abstraction. They work in time, material, and economic constraint. Collectors shape those constraints through consistent or inconsistent engagement.

artists being able to continue working

repeat collectors versus opportunistic buyers

price signaling and career stability

Financial participation creates either stability or volatility.

Speculation can increase visibility without sustaining practice. Rapid escalation can distort artistic trajectory as easily as neglect. Flipping behavior extracts value from the system it appears to support.

Artists are not passive in this structure. Some actively shape it by adjusting pricing, limiting supply, or pacing production to maintain control over their practice. Others adapt to institutional and market pressure.

Infrastructure is co authored, but uneven in leverage.

Financial behavior is a pattern, not a moment.

2. Preservation Infrastructure

If financial infrastructure determines what can be made, preservation infrastructure determines what remains.

archives

conservation

documentation

provenance

Without these systems, cultural production becomes temporary, even when it is significant.

If it is not preserved, it eventually did not happen.

Preservation is no longer only physical. It is increasingly digital, where fragility takes forms that are less visible but often more total in their impact.

This includes file decay, platform dependency, format obsolescence, and the gradual disappearance that occurs when technological ecosystems evolve faster than the works built within them. A video work tied to a deprecated codec, a generative artwork dependent on an outdated software library, or a web-based piece reliant on a discontinued server may continue to exist as files while becoming functionally inaccessible.

In this environment, collectors become custodians of access as much as objects.

Their responsibility is no longer limited to keeping a work. It extends to keeping it usable.

A digital artwork is only as stable as the systems it depends upon. Software, operating systems, hardware, networks, and storage environments form a chain of dependencies that must remain functional for the work to survive in any meaningful sense.

Preservation therefore becomes less about a single object and more about maintaining an ecosystem.

A work that cannot be migrated, displayed, interpreted, or reactivated across changing technological environments is effectively lost, even if the original file remains intact.

This shifts collecting from ownership toward continuity.

Preservation is what separates cultural memory from cultural disappearance.

And in digital contexts, disappearance is rarely dramatic. More often, it is procedural.

Works are not necessarily removed. They become unsupported.

The systems required to access them quietly vanish, one layer at a time, until the work remains technically present but culturally unreachable.

3. Visibility Infrastructure

If preservation determines what survives, visibility determines what is seen.

exhibitions

loans

placements

collector lending

Historically, visibility flowed through institutions. Museums, galleries, critics, curators, collectors, and publications largely determined what entered public consciousness.

That ecosystem still matters, but it no longer operates alone.

Today, visibility is increasingly shaped by algorithmic systems that reward attention, engagement, novelty, and repetition.

Social media has dramatically expanded access to audiences. Artists who might never have entered traditional institutional pathways can now build careers, communities, and collector bases directly. Entire generations of artists have found visibility through platforms that did not exist twenty years ago.

This expansion should not be dismissed. It has lowered barriers to entry, diversified participation, and created opportunities for artists at every stage of practice, including those who may never seek institutional validation.

At the same time, these systems introduce a new tension between visibility and significance.

Not all visibility carries the same weight.

Some visibility generates sustained engagement, patronage, scholarship, exhibitions, and collecting activity. Other forms produce the appearance of influence without creating durable support structures.

Social media can create both real visibility and pseudo visibility.

An artist may accumulate followers without collectors, attention without patronage, or engagement without meaningful opportunities. Visibility becomes measurable, but not necessarily transferable.

What matters is not visibility alone, but whether visibility converts into sustained forms of support.

Attention must become relationships.

Relationships must become patronage.

Patronage must become sustainability.

Without that conversion, visibility remains largely performative.

The contemporary artist navigates a landscape filled with aspiration, projection, and constant signals of success. Opportunity appears omnipresent, while the mechanisms required to transform visibility into a sustainable practice often remain opaque.

The challenge is not simply fragmentation.

It is interpretation.

Artists are asked to distinguish between attention and opportunity, audience and community, visibility and infrastructure.

Platforms further complicate this distinction because they do more than amplify work. They shape what is perceived as viable in the first place.

Algorithms influence which aesthetics gain traction, which narratives receive attention, and which forms of artistic labor become visible. Cultural perception is increasingly structured before institutions, collectors, or critics ever enter the conversation.

Collectors are embedded in infrastructures designed by intermediaries. Increasingly, artists are as well.

Visibility built on platforms is also contingent rather than owned. Audiences are often developed within systems that can change instantly through shifts in algorithms, policies, monetization structures, or platform relevance.

This creates a form of infrastructural dependency where visibility can expand rapidly without creating long-term stability.

And visibility does not always correspond to significance. Attention can simulate importance, while work of lasting significance remains structurally unseen.

This does not replace traditional visibility infrastructure. It layers on top of it.

Collectors, institutions, platforms, and audiences now operate within overlapping systems competing to determine what is remembered, what is supported, and what ultimately becomes part of cultural memory.

Circulation creates awareness.

Support creates continuity.

Visibility without supporting infrastructure does not accumulate into cultural memory.

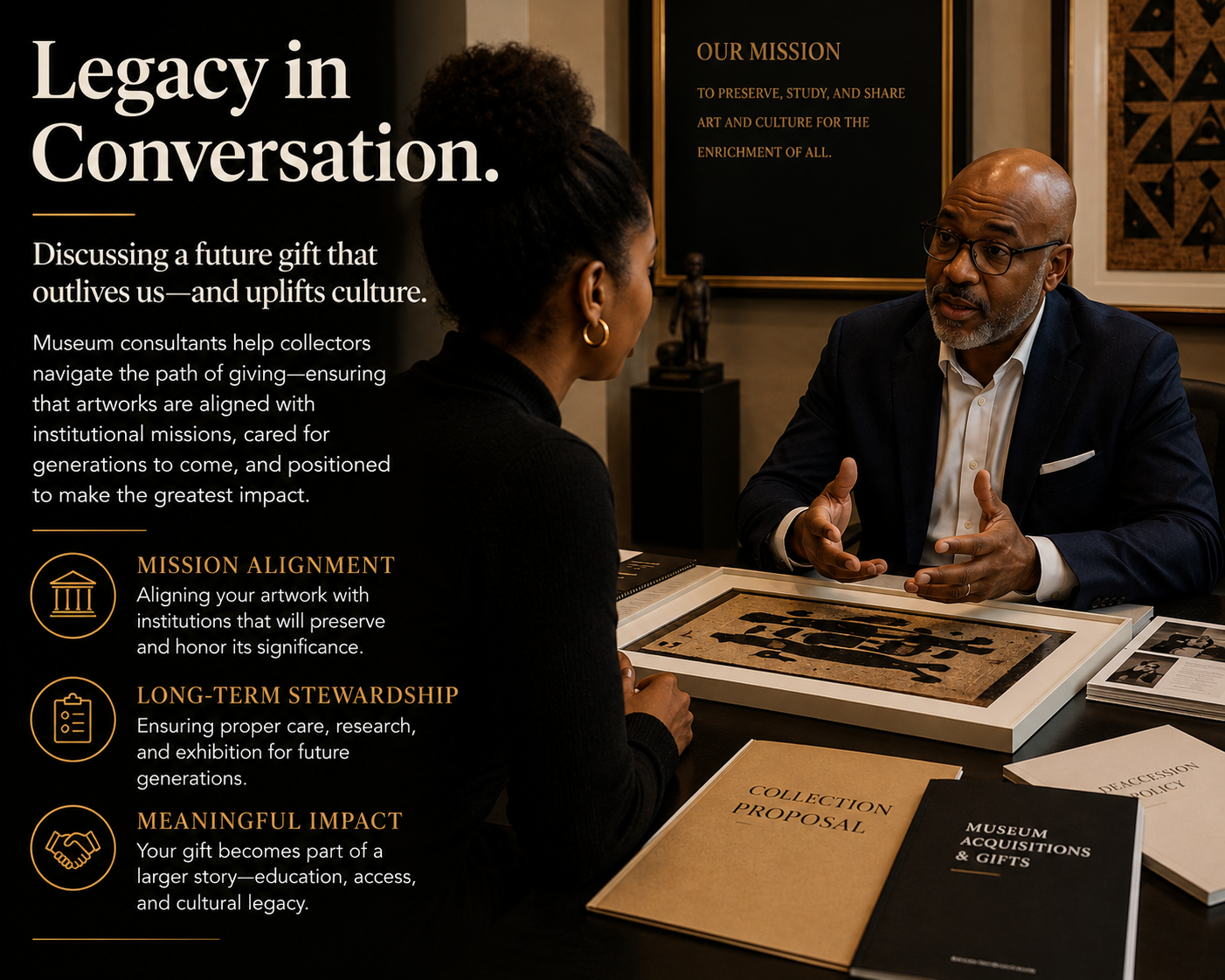

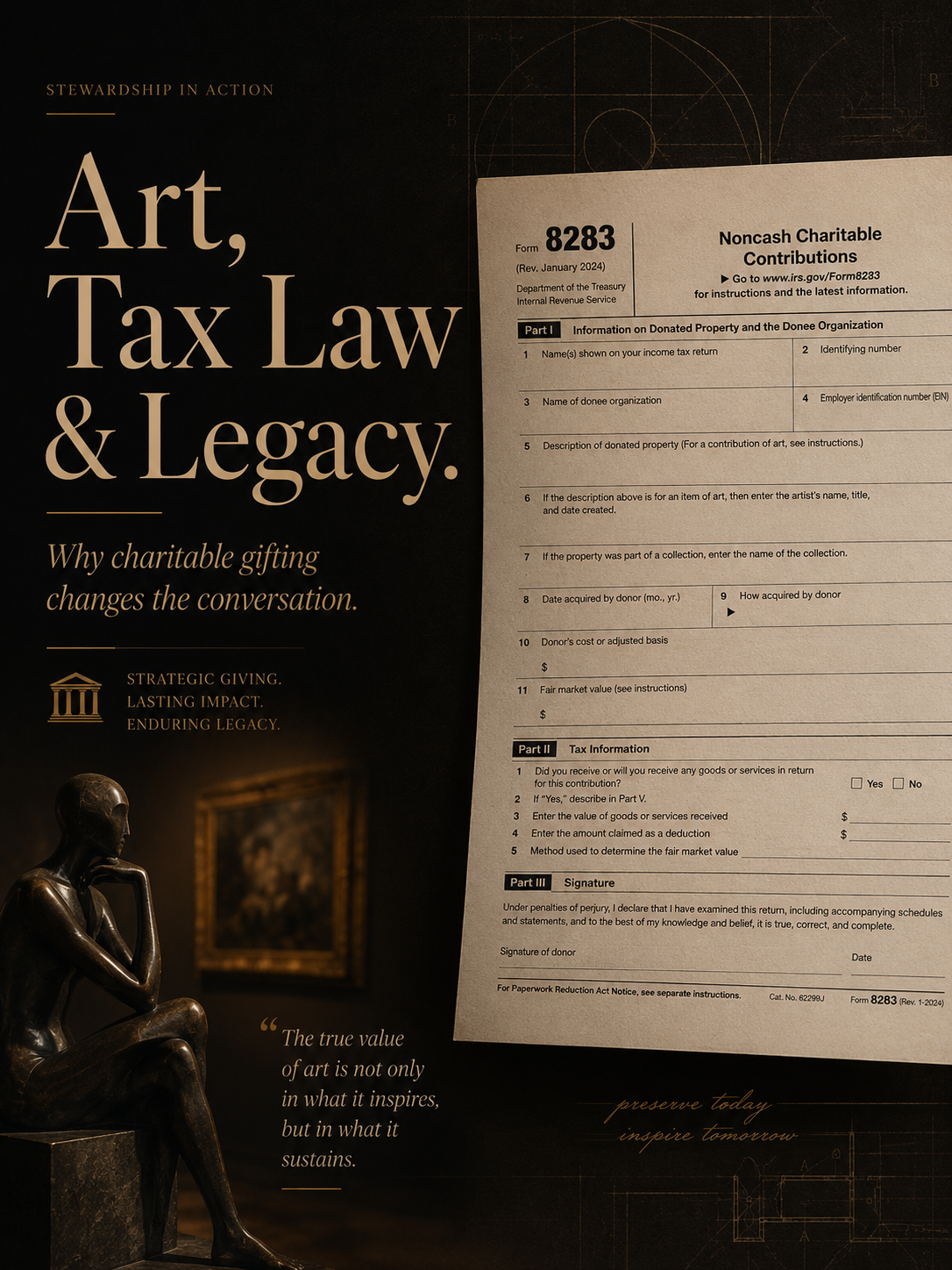

4. Legacy Infrastructure

The final layer is the one most often deferred.

estates

foundations

intergenerational transfer

long term stewardship

Legacy infrastructure determines what remains when ownership ends but cultural relevance continues.

Without it, even significant collections fragment or disappear.

There is a structural tension at its core.

Markets operate on short cycles. Cultural significance operates across generations. Collectors are incentivized toward immediacy while participating in systems that claim long term cultural impact.

Time determines whether cultural infrastructure compounds or collapses.

That mismatch is built into the system.

Legacy is not retrospective. It is infrastructural planning under time pressure.

Delay produces fragmentation.

Failure Modes: What Happens When Infrastructure Breaks

To understand infrastructure, it is necessary to understand failure as cultural consequence.

Financial failure leads to practices disappearing mid development

Preservation failure leads to histories becoming unverifiable

Visibility failure leads to narratives narrowing and repeating

Legacy failure leads to meaning being severed from context

Infrastructure is not neutral.

It can be fragile, extractive, or exclusionary.

When it fails, culture does not simply slow down.

It disappears in uneven and irreversible ways.

From Private Ownership to Cultural Responsibility

For much of modern history, cultural infrastructure was controlled through guilds, institutions, and closed systems that determined access, legitimacy, and preservation.

That structure has expanded, but its logic remains uneven.

Western institutions still dominate validation. Certain geographies and networks remain overrepresented in what is recognized as global culture.

Infrastructure concentration shapes cultural memory.

Collectors do not operate at equal scale, but they operate within the same system of accumulation, circulation, and preservation.

Collectors are influenced actors within infrastructures partially designed by intermediaries.

Galleries, advisors, and platforms do not simply participate in the system. They structure the conditions under which participation is possible.

As collecting becomes more distributed, responsibility becomes more distributed as well.

But influence remains uneven.

And infrastructure, by definition, is not symbolic.

It is consequential.

Closing Thoughts

Collecting is not the end point of cultural production.

It is part of its structure.

It is financial, preservation based, visibility driven, and legacy oriented, shaped by repeated decisions over time, mediated systems of influence, and uneven distribution of power.

The question is no longer whether collectors shape culture.

They do.

The question is whether they act with awareness of the infrastructure they are already building, and whether that infrastructure aligns with the cultural future it produces.

Bridging the Attention-Support Gap in the Contemporary Art World

If someone connects with an artist, supporter, or collector, they should not have to work to figure out what to do next. The clearer and simpler the next step, the more likely attention becomes action.

Most systems lose people at the moment of highest interest. Someone engages, feels something, then hits ambiguity with no clear button, no invitation, and no obvious path forward.

That gap quietly turns potential support into passive scrolling.

Build trust through consistent relationships, not one-off posts.

Sustainable support rarely comes from a single moment of resonance. It comes from familiarity built over time through repeated exposure, evolving context, and continuity with the artist’s world.

People do not just support what they like. They support what they understand. Understanding requires rhythm through updates, dialogue, and visibility beyond announcements.

When supporters feel like they are in relationship with the work, not just exposed to it, they move differently. They buy sooner, advocate more naturally, and stay longer.

Create clearer ways for collectors and supporters to act, whether to buy, commission, subscribe, or fund.

Interest without structure is leakage. Many artists generate attention but fail to convert it because the how-to-support layer is hidden, fragmented, or emotionally unclear. Support should not require interpretation. It should be legible in seconds. That means explicit pathways such as clear pricing, defined offerings, visible commissions, accessible subscriptions, and funding options that do not require decoding a system.

The easier it is to act, the less attention turns into hesitation.

Reduce dependency on platform visibility by adding owned channels, direct outreach, and diversified revenue streams.

Platforms can amplify reach, but they do not guarantee continuity. Visibility spikes are not stability. They are volatility disguised as opportunity. Sustainable creative careers require infrastructure that exists outside the feed, including email lists, direct collector relationships, recurring offerings, private communities, and non-algorithmic discovery systems.

The goal is not to abandon platforms, but to stop mistaking them for foundation.

Treat artists as workers and businesses, not just content producers, so the system includes pricing, systems, and sustained income. The dominant framing of artists as content generators removes the structural needs of long-term practice.

Sustainability requires operational thinking, including pricing that reflects labor and rarity, systems that reduce burnout, and revenue models that do not depend on constant visibility.

When art is treated as a business ecosystem rather than a stream of posts, stability becomes possible. The focus shifts from constant output to durable practice where income, time, and creative energy are actually aligned.

Sources: